Harnessing High-Interest Rate Opportunities For Wealth Growth

You have likely heard about the current buzz of high-interest rates, or you may have even felt their impact on your wallet. We are navigating a remarkable economic shift, moving from record-low interest rates to figures we have not seen in almost two decades—all within the span of just 18 months. In this short period, the landscape has dramatically changed: what was once an era of cheap and abundant debt has transformed into a climate where borrowing is expensive and securing loans can feel like scaling a mountain.

Just a few years ago, borrowers held the upper hand over lenders and savers. But the tables have turned, and now, lenders and savers have seized the advantage. What does this shift mean for you? It means that in the world of borrowing, higher interest rates now benefit the individuals who receive those interest payments, namely, the lenders and the savers. On the other hand, those who pay the interest rates, borrowers, have found themselves in a difficult and expensive situation.

As interest rates climb, the cost of borrowing follows suit, leading to heftier returns for banks, bondholders, and credit card companies on the money they lend out. But the benefits of these higher rates extend beyond just lenders. Savers also stand to gain, as higher interest rates mean that money parked in savings accounts, certificates of deposit (CDs), and money market funds are now working more efficiently for them. This uptick is thanks to financial institutions collecting higher interest income on newly issued loans, which then trickles down to savers in the form of improved returns.

Amid recent stock market volatility and concerns of an impending recession, investors and savers are grappling with where to allocate their funds. Driven by fears and uncertainty due to economic forecasts, many are seeking investment options that offer lower risk and more stable returns. This quest for financial safety is a direct response to the ongoing volatility in the broader economic landscape. Consequently, there is a growing focus on investment and savings strategies that prioritize the preservation of principal while still generating steady, reliable returns. While higher interest rates do bring their own set of challenges, they also usher in a range of opportunities for both investors and savers.

It is crucial to recognize these available opportunities. Despite the barrage of negative news about the economy and financial markets, opportunities for wealth growth are always there—you have to know where to look. Do not let negativity box you in; the financial landscape is a broad, fertile field brimming with opportunities to build and diversify your wealth. At Serene Financial Solutions, we are committed to shedding light on these opportunities and equipping you to capitalize on them for your long-term financial success.

Saving

Let's start by exploring savings. In years past, when interest rates were low, savings accounts were often viewed as mere holding vehicles for your money, offering negligible yields. But in today's high-interest rate environment, a variety of savings options have emerged that can significantly contribute to wealth accumulation. Depending on the type of account and the financial institution offering it, some savings accounts now boast yields of 6% or even higher.

High-Yield Savings Accounts, frequently available through online banks, offer a compelling avenue for individuals to both save and grow their money via competitive interest rates. These accounts distinguish themselves by offering significantly higher interest rates compared to traditional savings accounts, making them a go-to option for those seeking a low-risk place for their money to flourish. Furthermore, the interest in high-yield savings accounts is often compounded, meaning your money grows at an accelerated rate. To illustrate, a $10,000 deposit in an account with a 4.5% annual interest rate, compounded monthly, could generate approximately $460 in interest over the course of a year. With FDIC insurance, accessible online and mobile access, and withdrawal flexibility, these accounts are increasingly becoming the preferred choice for building emergency funds or meeting short-term savings goals.

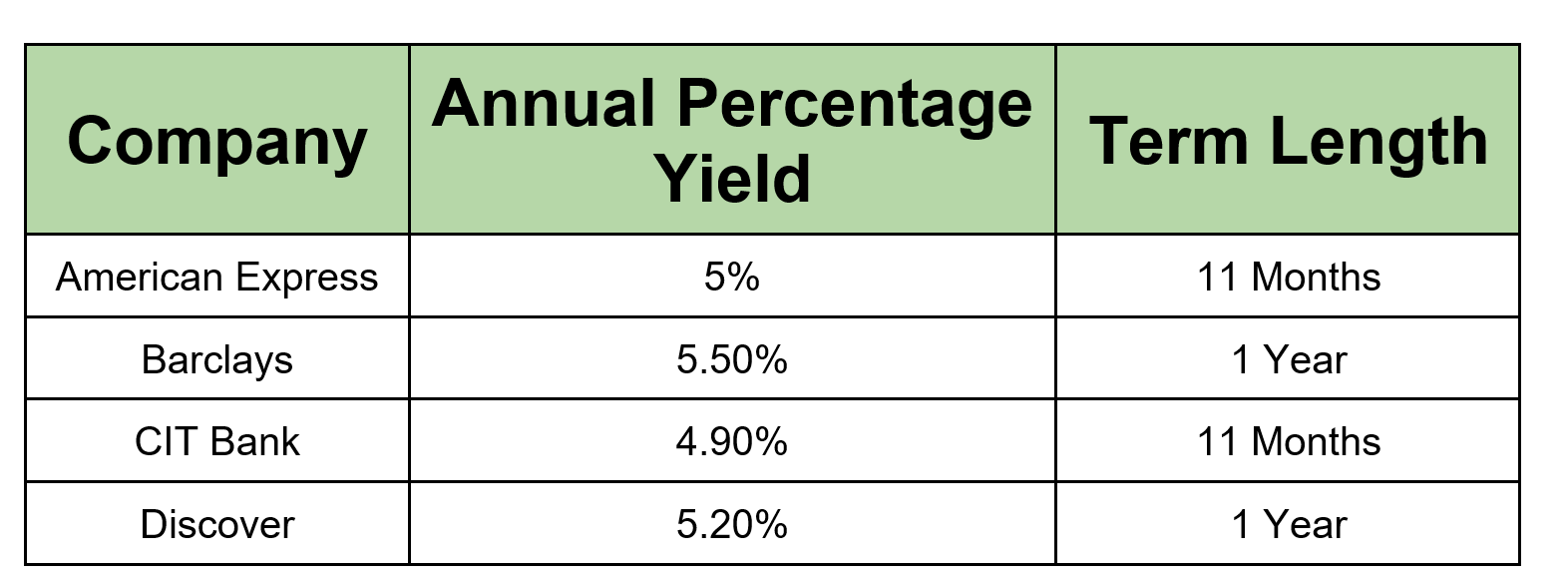

To provide an idea of what current yields are at different banks and financial institutions, here are a few.

Certificates of Deposit (CDs) offer yet another avenue for those in search of higher yields. These time-sensitive financial products require you to commit your funds for a specified period. Still, in return, they typically offer more appealing interest rates than regular savings or money market accounts. For example, a $15,000 investment in a 1-year CD boasting a 5% annual percentage yield would net you $750 in interest by year's end. Certificates of Deposit provide you the tangible sense that your money is actively working on your behalf, all while eliminating concerns about whether your investment is appreciating. However, given that CDs lock in your funds for the duration of the term, it is crucial to maintain a separate pool of readily accessible funds for immediate financial needs or emergencies. While CDs can be a potent source of low-risk, passive income, their limited liquidity should be a key consideration in your broader financial planning.

To provide an idea of what current yields are at different banks and financial institutions, here are a few.

Money Market Accounts offer a hybrid solution, blending the advantages of both savings and checking accounts. They generally provide more competitive interest rates than standard savings accounts while also offering the liquidity and easy access traditionally associated with checking accounts. Money market accounts operate by investing your deposited funds in a range of short-term, low-risk financial instruments like government securities. This setup allows you to benefit from higher yields while maintaining the flexibility to access your funds as needed.

To provide an idea of what current yields are at different banks and financial institutions, here are a few.

U.S. Savings Bonds, Such as the Series I and Series EE, serve as reliable options for those who prefer low-risk saving vehicles. Series I bonds offer a dual advantage: a fixed interest rate combined with an inflation-adjusted component, safeguarding your savings' purchasing power over the long term. At present, these bonds boast a rate of 5.27%, which includes a fixed rate of 1.30%. Series EE bonds offer a different approach, delivering a consistent fixed-rate return and a guarantee to double in value over a 20-year period. For instance, if you invest $5,000 in an EE bond today, you can rest assured that this initial deposit will grow to $10,000 within the next two decades.

Investing

Let's shift our focus to the world of investments. High-interest rates create a wealth of opportunities for those in search of stable returns. In an environment where riskier assets can experience dramatic value fluctuations daily, these investment options shine as a result of their reliability and stability.

When it comes to safety, U.S. Treasury Bonds are the gold standard. Backed by the faith and credit of the U.S. government, they are considered among the most secure investments available. In today's high-interest rate climate, Treasury bonds step into the spotlight by offering competitive yields, making them particularly attractive to investors seeking reliable passive income. When you invest in a Treasury bond, you become a lender to the American government, benefiting from consistent semi-annual interest payments and the return on your initial investment once the bond reaches maturity.

Interest Yields

Municipal Bonds present a compelling investment opportunity, particularly beneficial in today's high-interest rate environment. What sets these bonds apart from others are their remarkable tax advantages. While the interest yield on municipal bonds tends to be lower than on other bonds, such as Treasury bonds, the interest income earned from municipal bonds is typically exempt from federal income taxes, and if you invest in municipal bonds issued within your state, you will likely be exempt from paying state taxes as well. These tax benefits make municipal bonds especially attractive to investors in higher income tax brackets, significantly increasing their after-tax returns.

Corporate Bonds issued by companies offer a spectrum of credit quality that ranges from investment-grade (with a lower risk of default) to high-yield (with a higher risk of default). While investment-grade bonds may not have offered eye-catching returns in the past, the current high-interest rate environment has shone a spotlight on them. They now provide relatively robust returns while maintaining a degree of safety. In essence, these bonds facilitate a partnership between investors and corporations: investors lend capital to companies in exchange for regular interest payments and the return on their initial investment. Suppose you opt for a bond from a financially stable, creditworthy company. In that case, the odds are good that you will receive your scheduled payments, albeit at a lower interest rate. Conversely, those seeking higher yields may find themselves considering bonds from less creditworthy firms, which carry a substantially greater risk of default on both interest and principal repayments.

These were September's monthly average yields for high-quality market corporate bonds, bonds issued by well-established, financially stable companies with a low risk of default.

In today's high-interest rate environment, challenges and opportunities abound. While borrowers may feel the pinch, this climate is ripe with potential for savers and investors. For starters, do not overlook the power of high-yield savings accounts, CDs, and U.S. Savings Bonds to boost your earnings—each serves different needs and risk appetites, so choose what fits you best. When it comes to investments, diversification is your friend. Balance your portfolio with a mix of U.S. Treasury bonds for safety, municipal bonds for tax advantages, and corporate bonds for higher yields with a moderate level of risk. Tip: If you are in a higher tax bracket, those municipal bonds can be incredibly lucrative for you. Another tip: Be mindful of your liquidity needs when opting for CDs or certain kinds of bonds that lock in your money for an extended period. The takeaway here is to be proactive and strategic. By recognizing and seizing these high-interest opportunities, you are not only protecting your financial well-being but setting the stage for meaningful wealth growth. In uncertain times, these strategies can serve as your financial anchor, helping you navigate choppy waters with confidence.

Disclaimer: The information provided in this article is for informational purposes only and does not constitute financial or tax advice.